A highly desirable hybrid vehicle appears on a digital salvage auction. It features low mileage, a seemingly minor damage category, and a current proxy bid that makes trade calculators smile. However, there is a critical financial question that is rarely advertised in bold letters across the listing description: what exactly happens to that immensely expensive battery coverage once the insurance assessor officially writes the car off?

Far too many inexperienced buyers celebrate securing a bargain hybrid purchase only to discover six months later that the manufacturer support is entirely void, the dashboard is illuminated with high-voltage warning lights, and the replacement cost exceeds what they paid for the entire chassis. A primary hybrid battery warranty does not automatically follow the vehicle through the salvage ecosystem. Understanding this highly specific legal and financial reality before committing your working capital could save your business thousands of pounds. Whether you are a trade buyer sourcing efficient urban runabouts or an independent mechanic seeking a profitable project, the legal status of the battery matters significantly more than the condition of the exterior paintwork.

What Happens to Manufacturer Warranties After Write-Off

When an insurance company declares a vehicle a total loss and assigns a formal salvage category, the direct relationship between the manufacturer and that specific vehicle is permanently altered. Most major hybrid manufacturers, including Toyota, Honda, Hyundai, and Lexus, strictly tie their battery guarantees to the vehicle's legal status and its unbroken ownership history.

The clinical reality is that the vast majority of manufacturer warranties become entirely void the exact moment an insurance company formally writes the vehicle off. It typically does not matter if the collision resulted in purely cosmetic damage or severe structural distortion. Warranty terms universally include strict clauses regarding total loss declarations, and insurance databases automatically notify manufacturers when these claims are settled.

Toyota, for example, offers an incredibly robust 15-year warranty on many of its hybrid models. However, the small print dictates the commercial reality. That specific coverage applies exclusively to vehicles maintained within their approved dealer network that have never been subjected to an insurance write-off. Once a pristine Prius receives a salvage marker, Toyota's legal obligation to replace degraded cells almost always terminates immediately. Expecting a seamless salvage warranty transfer simply because the previous private owner had time remaining on their contract is a guaranteed route to financial disappointment. Buyers must operate under the strict assumption that they are purchasing the asset completely "as-seen," with absolutely zero manufacturer backing.

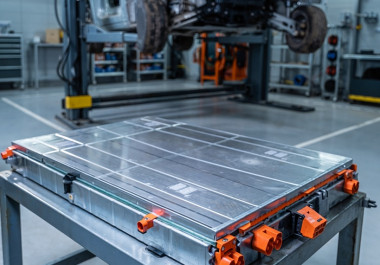

How Salvage Categories Affect Battery Coverage

The specific salvage category stamped on the DVLA database affects significantly more than just your future insurance premiums. It directly dictates whether any form of coverage, be it from the manufacturer or a third-party underwriter, will ever touch the high-voltage pack again.

Category S vehicles present the steepest operational challenges. These vehicles have sustained structural damage to the main chassis or frame. Manufacturers logically argue that heavy structural impacts might have subtly warped the battery mounting points, severed complex cooling systems, or stressed the high-voltage electrical connections in ways that will not manifest for thousands of miles. Even if the structural damage was isolated entirely to the front crumple zone and nowhere near the rear-mounted battery, the Category S marker frequently triggers an automatic, non-negotiable warranty exclusion. Furthermore, you must explicitly remember that Category B vehicles are strictly reserved for licensed Authorised Treatment Facilities (ATFs) for parts reclamation only; they can never return to the road, meaning warranty discussions are entirely irrelevant.

Category N vehicles, which feature non-structural cosmetic or electrical damage, fare slightly better in the negotiation room, but only marginally. Occasionally, manufacturers will review claims on Category N vehicles if the buyer can definitively prove the damage was completely unrelated to the hybrid drivetrain. For instance, light interior fire damage or recovered theft vehicles with shattered windows might leave a tiny margin for negotiation, provided the buyer can supply impeccable service history and proof of manufacturer-approved repairs.

Transferring Existing Warranties: What Works

Trade buyers determined to salvage some form of coverage face highly limited, exceptionally strict options. Understanding what actually works versus what is legally impossible helps set realistic operational expectations before the auction timer expires.

Extended policies purchased by the previous owner are functionally useless. Mainstream companies offering extended coverage almost universally bury clauses in their terms and conditions explicitly excluding any vehicle bearing a salvage marker. The policy dies with the insurance claim, regardless of whether three years of premium coverage remained. Expecting a successful salvage warranty transfer from a consumer protection policy is entirely unrealistic.

Manufacturer goodwill represents the absolute best potential route, although it is never guaranteed. If a hybrid develops a battery fault that is clearly, undeniably a factory defect entirely unrelated to the auction damage, some manufacturers will occasionally authorise a goodwill repair to protect their brand reputation. To maximize the chances of this rare outcome, buyers must rely heavily on pristine documentation. You must secure all previous digital service records, ensure the vehicle is inspected by a certified high-voltage technician immediately upon extracting it to your workshop, and officially register the asset under your commercial trade account or business fleet profile with the manufacturer.

Third-Party Battery Warranties for Salvage Hybrids

Because the original factory protection typically vanishes the moment the digital hammer falls, buyers often look toward third-party coverage. While this niche market is growing, it remains highly fragmented, restrictive, and exceptionally expensive for commercial operators.

Most trade buyers bypass consumer-focused aftermarket policies entirely. Instead, they rely on localized, trade-only agreements with specialist battery refurbishers, factoring the wholesale cost of a reconditioned pack directly into their initial proxy bidding equations.

This more realistic approach relies purely on component guarantees. Independent suppliers frequently provide their own robust 12 to 24-month warranties on their specific reconditioned units. This completely bypasses the manufacturer and provides genuine commercial peace of mind, provided you accurately mathematically budgeted for the unit from day one.

What to Check Digitally Before Bidding

Because secure salvage compounds strictly prohibit physical public yard browsing for severe health and safety reasons, you cannot simply plug a diagnostic scanner into the OBD port before bidding. You must rely entirely on rigorous digital inspection techniques to determine if the high-voltage system is likely to survive without coverage.

Your absolute first priority is scrutinising the dashboard photography. Zoom in heavily on the instrument cluster when the ignition is illuminated. Any visible hybrid system warning lights, red triangles, or "Check EV System" messages are immediate, massive red flags. Next, cross-reference the vehicle's age against its mileage. Hybrid batteries degrade based on both time and usage, but vehicles displaying exceptionally low annual mileage often suffer worse battery degradation because the cells are not cycled and conditioned regularly.

The public DVLA MOT database is your most valuable digital tool. Review the historical advisories meticulously. A clean current MOT does not guarantee a healthy battery, but a historical string of advisories mentioning electrical faults, warning lights, or hybrid system errors should prompt you to walk away immediately.

Regional Variations and Manufacturer Policies

Warranty policies and specialist support networks are not uniform across the UK. Depending on where you operate, repairing a complex hybrid without manufacturer support can range from a minor inconvenience to a logistical nightmare.

Toyota and Lexus operate a massive UK network and are generally considered the most flexible regarding goodwill claims on Category N vehicles, particularly if you can digitally prove the damage was purely cosmetic. Conversely, Honda takes an exceptionally hard line on salvage titles. Their internal policies explicitly exclude any vehicle bearing an insurance write-off marker from high-voltage coverage, leaving absolutely zero room for negotiation. If you are sourcing stock from standard car auctions uk platforms, buying a salvage Honda Jazz hybrid means assuming absolutely zero corporate support.

Hyundai and Kia offer highly attractive 7-year or 100,000-mile factory warranties, but these are instantly voided upon salvage categorisation. However, their independent specialist network is growing rapidly, making affordable aftermarket repairs increasingly viable. Premium marques like BMW and Mercedes are entirely inflexible; their systems are immensely complex, and repairing them outside the main dealer network requires highly specialised, expensive software access.

The Real Cost of Buying Salvage Hybrids Without Warranty

This entire process ultimately reduces to clinical mathematics. A salvage hybrid lacking coverage must be acquired cheaply enough that the absolute worst-case scenario remains financially viable. You must calculate the exact cost of replacing the battery before you place a bid.

Replacement costs vary wildly. A new factory pack for a third-generation Toyota Prius might cost £3,000, while a refurbished unit sits around £1,500. A replacement battery for a premium plug-in hybrid SUV can easily exceed £6,000. Labour adds another £300 to £600 rapidly, as high-voltage systems require IMI Level 3 certified technicians utilizing insulated tooling. When browsing vast catalogues of salvage cars, your maximum bid must reflect this specific risk.

If you are evaluating a Category S hybrid for £4,000 when an unrecorded retail example costs £7,000, your theoretical margin is £3,000. If the battery fails the following week, that entire margin is instantly wiped out. That is not a strategic business investment; that is a blind gamble. Conversely, if you apply the exact same risk assessment principles used when sourcing inventory from a motorcycle auction and secure that vehicle for £2,000, you retain a massive £5,000 financial buffer. Even if the battery requires total replacement, you still extract a profitable margin.

Making the Decision: When Salvage Hybrids Make Sense

After analyzing thousands of digital lots, the commercial reality is crystal clear. Operating without a hybrid battery warranty makes perfect financial sense if you are acquiring the asset at 40 to 50 percent below its clean market value and possess the liquid cash reserves to absorb a catastrophic cell failure.

This sector works brilliantly for trade buyers who already possess deep relationships with independent battery refurbishment specialists. It works exceptionally well for confident mechanics who understand high-voltage safety protocols and can swap a battery pack in their own workshop, completely eliminating external labour rates. If an asset ultimately proves entirely unviable due to deep, hidden electrical faults, smart operators know they can utilize a rapid scrap my car valuation to liquidate the raw materials and mitigate their exposure.

However, this market is entirely unsuitable for private buyers seeking a reliable, cheap daily commuter. It is unsuitable for buyers operating on strict, inflexible budgets who cannot afford a sudden £2,000 repair bill. If you are relying on the hope of a successful manufacturer claim to make your spreadsheet work, you are bidding on the wrong vehicle auction lot. Furthermore, buyers must always remember that the original V5C logbook is frequently missing in salvage sales. You must proactively factor in the time delay of submitting a V62 application form to the DVLA alongside running your own mandatory independent HPI checks to ensure the asset is free of outstanding finance.

Conclusion

Hybrid vehicles and salvage categories do not mix harmoniously, and pretending otherwise is a highly expensive mistake. Manufacturer obligations typically vanish the precise moment the insurance assessor finalises the write-off, regardless of whether the damage was structural or a minor cosmetic scrape. Third-party coverage is restrictive, expensive, and frequently excludes previously damaged chassis entirely.

Your absolute best protection is not an extended policy; it is clinical knowledge, realistic mathematical budgeting, and a ruthless digital assessment of the vehicle before you submit a proxy bid. Assume you have zero corporate support, calculate the cost of a full replacement, and only proceed if the numbers still represent genuine commercial value.

The RAW2K platform provides highly detailed photography and transparent category markers, allowing educated buyers to spot incredible, high-margin opportunities that terrified the broader retail market. If you require any specific guidance regarding hybrid lot descriptions or navigating the secure compound collection rules, please don't hesitate to contact us. To begin actively sourcing profitable, modern hybrid inventory for your business, create your profile and register to bid today.